Nimble MSME Loan Solution – A Winning Formula for MSME Lending

The Indian MSME sector, the lifeblood of our economy faces a familiar challenge: access to credit. Traditional methods rely heavily on credit history, a hurdle for young businesses. Here’s where Craft Silicon’s Nimble Business Loan Origination System steps in, offering a powerful solution with industry-specific cash flow analysis to revolutionize MSME lending in India.

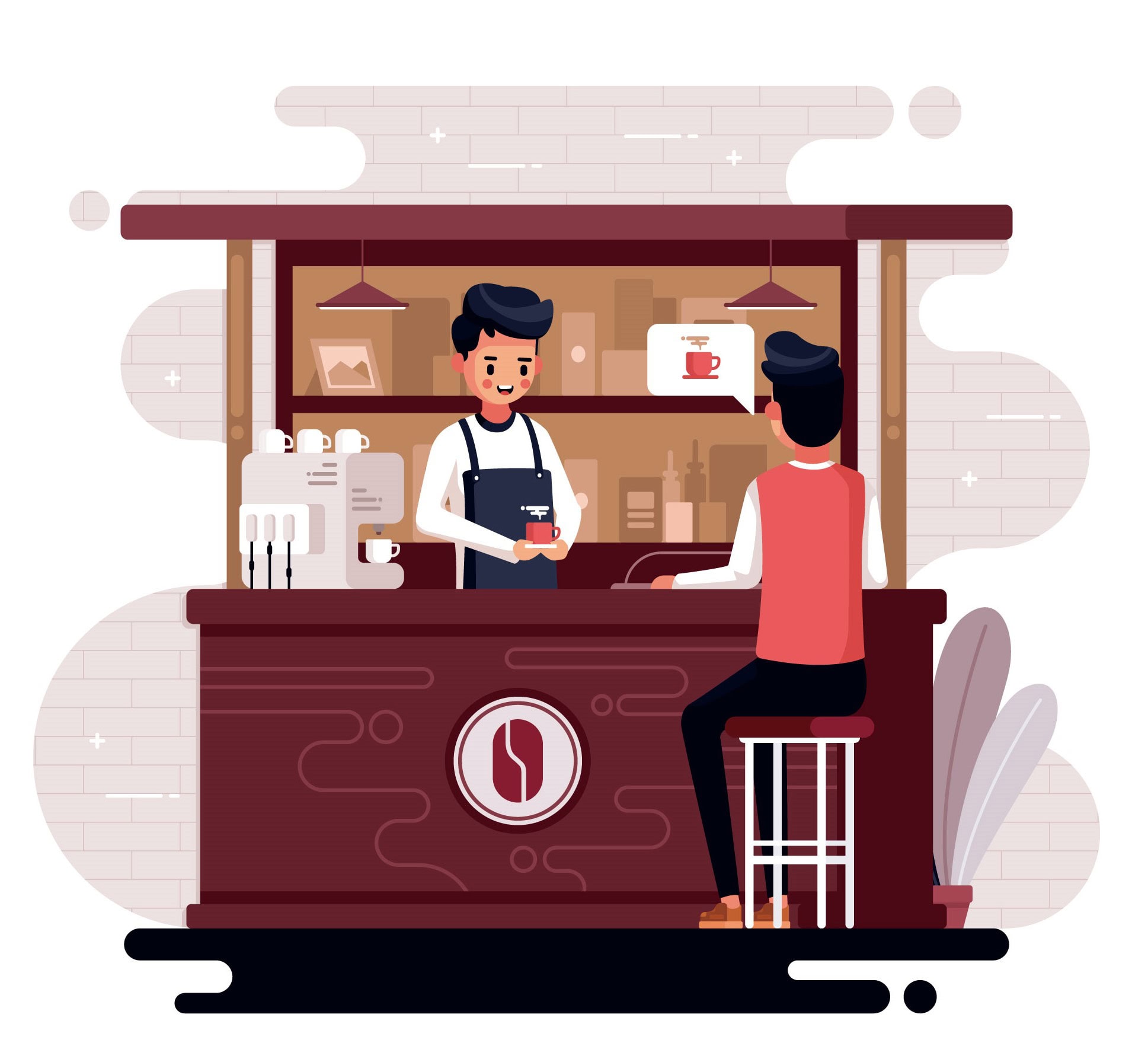

Imagine Ravi, a chaiwallah at the end of the street busily brewing tea/coffee in his shop. He looks to get a business loan to expand his tea shop into a coffee café. While Ravi lacks a long credit history, his consistent customer flow and daily sales paint a clear picture of his cash flow potential. Nimble empowers lenders to go beyond basic credit history. They can configure a custom cash flow analysis template specifically designed for chaiwalas. This template might include questions like:

-

- Daily Sales: How many cups of tea, coffee, Horlicks do you sell in the morning, afternoon, and evening?

- Pricing: What’s the cost per cup?

- Operational History: How many days per month do you operate?

Nimble then gathers Ravi’s responses and combines them with industry benchmarks to generate a customized cash flow forecast. This forecast considers seasonal fluctuations and peak hours, providing a clearer picture of Ravi’s earning potential.

Imagine Ravi, a chaiwallah at the end of the street busily brewing tea/coffee in his shop. He looks to get a business loan to expand his tea shop into a coffee café. While Ravi lacks a long credit history, his consistent customer flow and daily sales paint a clear picture of his cash flow potential. Nimble empowers lenders to go beyond basic credit history. They can configure a custom cash flow analysis template specifically designed for chaiwalas. This template might include questions like:

- Daily Sales: How many cups of tea, coffee, Horlicks do you sell in the morning, afternoon, and evening?

- Pricing: What’s the cost per cup?

- Operational History: How many days per month do you operate?

Nimble then gathers Ravi’s responses and combines them with industry benchmarks to generate a customized cash flow forecast. This forecast considers seasonal fluctuations and peak hours, providing a clearer picture of Ravi’s earning potential.

Nimble: Unlocking the Potential of Every MSME with Unmatched Flexibility

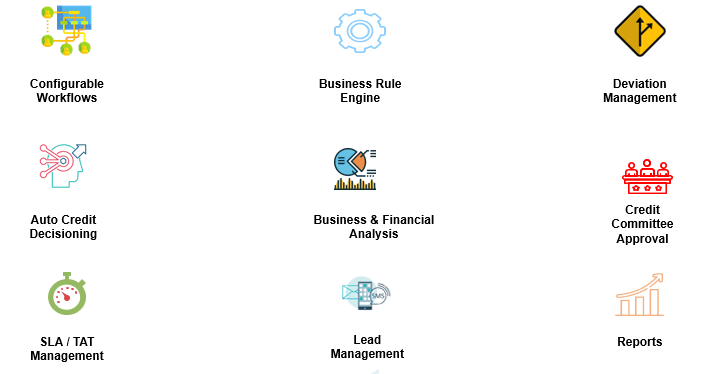

Nimble empowers lenders (banks and NBFCs) with the tools they need to thrive in the new era of MSME lending:

- Configurable Cash Flow Analysis: Nimble allows lenders to design industry-specific cash flow analysis templates. These templates capture the unique income and expense structures of different MSME sectors (e.g., chaiwalas vs. tailors vs grocery shop owner).

- Data-Driven Decisions: Nimble goes beyond cash flow analysis. It integrates with credit bureaus and allows lenders to configure risk-based pricing models based on factors like CB score, average monthly balance, and repayment history.

- Internal Credit Scoring: Nimble empowers lenders to develop their own internal credit scoring systems for MSMEs. These systems consider multiple parameters relevant to an MSME’s industry, like Ravi’s daily sales volume or a tailor’s average order value.

- Multi-Level Loan Approval: Nimble supports a customizable loan approval matrix based on both internal credit score and loan amount. This allows lenders to streamline approvals while maintaining appropriate risk management.

Enhanced Configurability and Risk Management:

- In-House Dynamic Business Rule Engine (BRE): Nimble offers a powerful BRE system. Lenders can configure rules for various aspects like KYC verification, loan origination, loan servicing, credit bureau checks, and more. This ensures compliance and streamlines processes.

- Well-Defined Deviation Approval Matrix: Nimble allows for multi-level approvals when system deviations or manual overrides occur. Deviation-wise approval roles (business, risk, credit, etc.) can be configured for granular control.

Seamless KYC and Financial Assessment:

- Bank Statement Analysis: Nimble analyzes the borrower’s past 6 months of bank statements, providing a consolidated view of their cash flow. This complements the customized cash flow analysis for a holistic financial picture.

- KYC Authentication: Nimble supports Aadhaar offline KYC, PAN verification, and voter ID authentication for secure and efficient KYC checks.

- MSME Udyam Integration: Nimble seamlessly integrates with the MSME Udyam registration system, allowing lenders to fetch Udyam certificates for faster loan processing.

Benefits for Lenders:

- Expanded Reach: Confidently tap into the vast potential of the MSME sector with tailored cash flow analysis for each industry.

- Reduced Risk: Data-driven decisions based on comprehensive financial health assessments lead to better loan performance and reduced risk exposure.

- Competitive Advantage: Offer innovative loan products with risk-based pricing and cater to the specific needs of diverse MSMEs.

- Increased Efficiency: Streamlined processes, automation, and a powerful BRE significantly improve operational efficiency for lenders.

- Enhanced Risk Management: Granular control over approvals and dynamic rule configuration ensure compliance and mitigate risk.

Ready to unlock the power of Nimble for your MSME lending? Contact Craft Silicon today!

Author: Sriram Ganesan | AVP – Product and Pre-sales

Sriram is a certified PMP and CAIIB professional having more than 18 years of experience in the banking domain (retail and corporate) that spans into product management, presales, business analysis, project management . He has worked in largescale transformation projects for global banks. He has rich experience in lending domain and has played key role in launching Nimble product suite for Craft Silicon. He is a fintech enthusiast interested in learning and sharing fintech knowledge to the community. Sriram is currently leading the product management practice at Craft Silicon.