The Evolution of Co-lending

Co-lending has significantly evolved over the years, revolutionizing the way financial institutions collaborate to fund projects and businesses. Understanding the roots and importance of co-lending is crucial to understanding its current impact on the financial sector. Co-lending plays a fundamental role in promoting financial inclusion by providing access to capital for individuals and businesses that may not meet traditional lending criteria. It fosters innovation, enables priority sector like MSME, and facilitates economic growth.

What is Co-lending?

Co-lending involves collaboration between two types of partners: the Financing partner and the Servicing partner.

- Financing Partner(FP): This partner contributes a larger percentage of the loan amount in the partnership. They provide the bulk of the capital needed for the loan.

- Servicing Partner(SP): This partner is responsible for servicing loan to customer. Their roles include primary sourcing of the loan, managing loan repayments(collections), & acting as the main point of contact for the customer throughout the loan process.

In this arrangement, the financing partner ensures the availability of funds, while the servicing partner handles the operational aspects of the loan, ensuring smooth management and repayment. This collaboration allows for the pooling of resources and expertise, leading to more efficient and inclusive lending practices.

History of Co-lending

The concept of co-lending dates back to ancient civilizations, where groups of individuals would pool resources to support fellow community members in need. Fast forward to modern times, banking institutions began formalizing co-lending practices to cater to diverse financial requirements.

Reserve Bank of India (RBI) Guidelines

The RBI has issued guidelines to formalize co-lending arrangements, particularly between banks and non-banking financial companies (NBFCs). The Co-Lending Model (CLM), introduced in 2020, aims to enhance credit flow to priority sectors by leveraging the comparative advantages of banks and NBFCs.

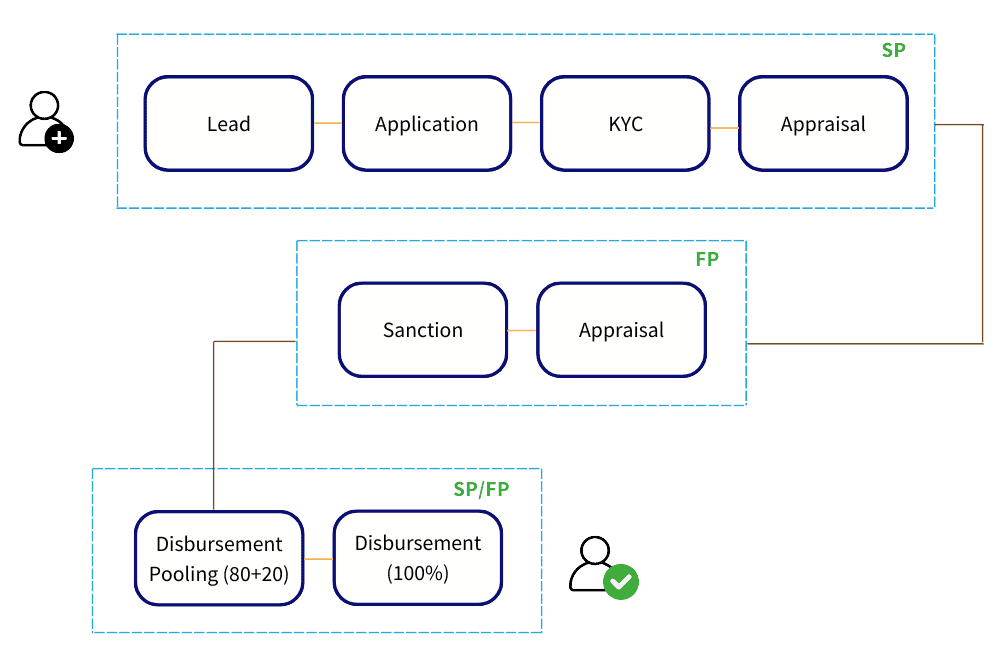

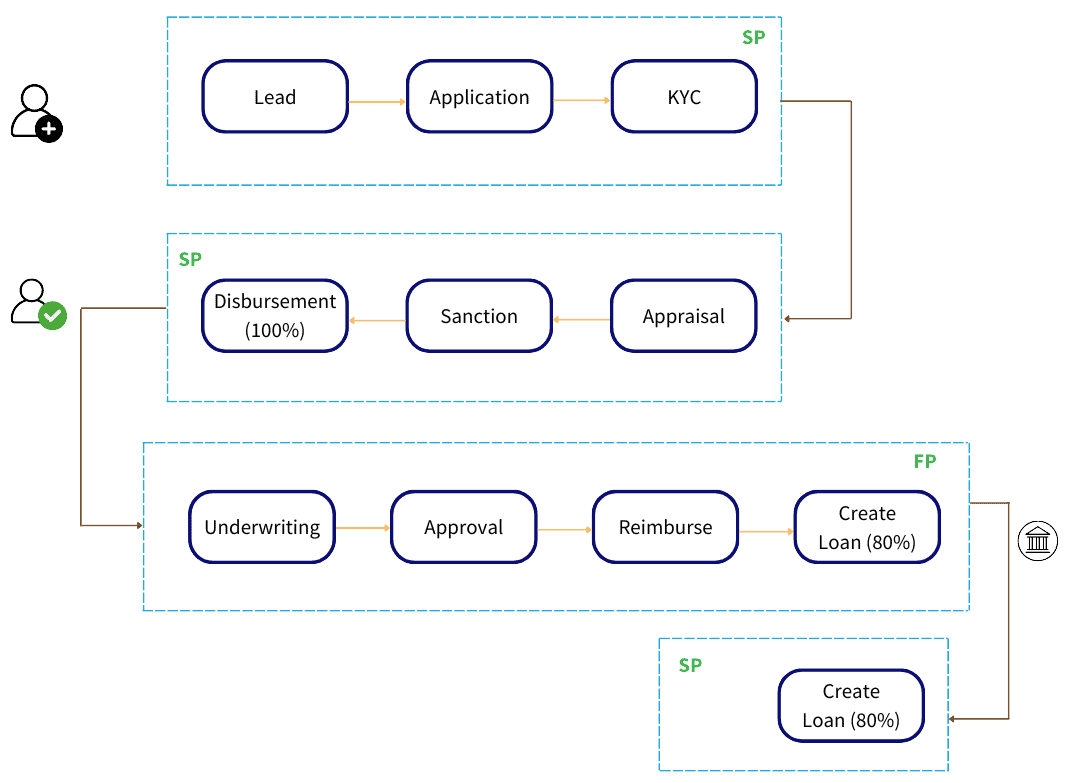

Types of Co-lending Models

- CLM 1 – In this model, all the co-lenders jointly fund the loan amount according to pre-agreed ratios.

For example, Lender A funds 80% while Lender B funds 20% of the total loan amount.

- CLM 2- Reimbursement-based Co-lending- Here, one lender disburses the full loan amount first. Subsequently, the other lender reimburses a percentage of the loan, say 80%, to the first lender as per the co-lending agreement. This model is similar to Direct Assignment.

![]()

Benefits of Co-Lending

Co-lending offers numerous advantages for lenders, borrowers, and the overall financial ecosystem.

- Risk Diversification- By spreading loan exposure across lenders, co-lending significantly reduces the risk of any single lender facing substantial losses. This diversification strategy enhances financial stability and resilience.

- Increased Loan Approvals- Co-lending increases the likelihood of loan approvals for borrowers, especially those with unique or complex financing needs. Two lenders bring diverse perspectives and expertise to evaluate loan applications, leading to more inclusive lending practices.

- Lower Interest Rates for Borrowers- Collaborative lending often results in competitive interest rates for borrowers, as lenders work together to offer attractive terms and conditions. This fosters healthy competition in the lending market, benefiting borrowers with cost-effective financing options.

For Example:

Consider a co-lending partnership involving two lenders:

Lender A has an interest rate of 18% and contributes 80% to the loan amount. Lender B has an interest rate of 14% and contributes 20% to the loan amount. The blended rate of interest for the customer can be calculated using the following formula will be 17.20%

Formula : (Funder A Share % * Interest Rate of Funder A) + (Funder B Share % * Interest Rate of Funder B)

Using the given percentages and interest rates:

Blended Rate of Interest = (0.80×18%) + (0.20×14%)

Blended Rate of Interest = 14.4% + 2.8%

Blended Rate of Interest = 17.2%

![]()

Challenges of Co-lending

Despite its benefits, co-lending comes with its set of challenges that require careful consideration and strategic management.

- Coordination and Communication Issues- Coordinating two lenders, aligning on terms, and maintaining effective communication throughout the lending process can be challenging. Ensuring transparency, clarity, and accountability among all parties is essential to overcoming these hurdles.

- Credit Risk Management- Managing credit risk in co-lending arrangements demands robust credit assessment, monitoring mechanisms, and risk mitigation strategies. Lenders need to evaluate borrower creditworthiness, set appropriate risk limits, and monitor loan performance diligently to safeguard their financial interests.

- Technology Integration- Advancements in financial technology (FinTech) are revolutionizing co-lending processes, enabling digital platforms for seamless loan origination, underwriting, and servicing.

![]()

Solution for the challenges

Our Nimble co-lending system provides an effective solution by handling communication and balance management between both partners. Nimble co-lending acts as an intermediary, facilitating smooth interactions and operations between the serving partner and the financing partner.

- Enhanced Coordination and Communication: Nimble co-lending ensures effective communication channels between lenders, promoting transparency and clarity. The system provides a centralized platform for sharing information, aligning on terms, and tracking progress, thereby minimizing coordination issues.

- Improved Credit Risk Management: By monitoring Nimble co-lending helps in conducting thorough credit assessments and setting appropriate risk limits. It continuously monitors loan performance, offering real-time insights to both partners, which aids in proactive risk mitigation.

- Seamless Technology Integration: Nimble co-lending pulls progressive solutions to loan origination, underwriting, and servicing. This integration streamlines processes, reduces manual efforts, and enhances operational efficiency, making co-lending more effective and scalable.

Through these features, Nimble co-lending plays a pivotal role as a middle layer, ensuring smooth collaboration between the serving and financing partners, ultimately leading to a more efficient and effective co-lending process.

Summary

Co-lending provides risk diversification, increased loan approvals, and competitive interest rates while requiring effective coordination, regulatory compliance, and credit risk management.

- Lenders can mitigate credit risk by conducting thorough credit assessments, setting risk limits, and implementing robust monitoring mechanisms.

- Borrowers benefit from increased loan approvals, competitive interest rates, and access to diverse funding sources through co-lending.

- Technology integration enables automation, data analytics, and digital platforms for seamless loan origination, underwriting, and servicing in co-lending.

![]()

Author: Roopesh Kumar M | Associate Business Analyst, BA Solution

Roopesh is an Associate Business Analyst at Craft Silicon, with two years of experience in the company. He specializes in financial technology integration and is dedicated to enhancing financial inclusion and operational efficiency through innovative solutions in the banking sector. At Craft Silicon, Roopesh works in new product development, focusing on lending and banking solutions.